Every day is independence day for home buyers and sellers. Every day more consumers are freeing themselves from the deceptive business practices that so often lead to uninformed and bad decisions when it comes to buying or selling a home. That means that more consumers are seeking out conflict free real estate professionals whose advice is not marred by secret incentives that undermine the very reason those professionals were hired.

In the spirit of independence, CAARE is releasing this list of the top 10 worst business practices and how to avoid them. It is CAARE’s mission to empower consumers to make intelligent and informed real estate decisions and free themselves from bad practices when buying or selling a home.

Free Yourself from the Top 10 Worst Business Practices

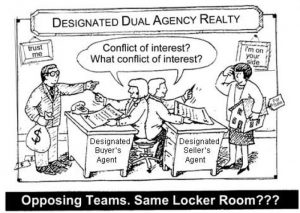

1. Dual Agency (click here for the article). This is the most deceptive and anti-consumer practice – avoid at all costs. No one can serve two masters and when they do the conflicts are on the verge of absurd and usually insurmountable. Dual agency occurs when the brokerage firm represents the buyer and seller on the same transaction (even if different agents are involved). Dual agency arises with little warning and results in the abandonment of the services for which the agent was hired. In a dual agency, the broker gets paid double and the buyer and seller forfeit their right to representation on such things as negotiation of price and terms (2 of the top 3 reasons consumers hire Realtors*).

Solution. Look for quality agents from small brokerages or from brokerages that exclusively represent buyers or sellers. Never call on real estate advertisements or visit open houses.

2. Controlled Business Arrangements with Title and Closing Services (click here for story). Title companies that are owned or affiliated with other real estate professionals destroy the integrity of this vital check and balance. In addition, they destroy the consumer advantages that are borne by competitive business practices such as good service and competitive pricing.

Solution. (click here for our growing list of independent title agents). Only hire a title company that is truly independent of your brokerage, builder, lawyer or lender firm. Never use an affiliated business in real estate.

3. Lawyers Who Sell Title Insurance. Attorneys cannot negotiate title coverage on behalf of their client when the attorney also represents the title underwriter providing that coverage. In addition, the commission paid to attorneys on the sale of title insurance is very large and is only paid if the transaction closes interfering with the attorney’s representation of the clients’ best interests.

Solution. Hire an attorney whose practice focuses on real estate and who will not sell you or your lender title insurance.

4. Lawyers Who Represent Home Buyers, Sellers, and Who Also Represent or Receive Referrals From Real Estate Professionals. Many of the worst business practices will not be disclosed to buyers and sellers if the attorney represents, seeks to represent or gets referrals from real estate professionals.

Solution. Only hire a real estate attorney who does not represent or get referrals from real estate professionals.

5. Marketing Manipulation That Fosters Dual Agency. Many real estate brokerages engage in market manipulations disguised as selling strategies. These practices usually involve limiting demand in order to collect a double commission.

a. Pocket listings (aka Sneak Peaks) (click here for story). Properties are shown only to in-house agents prior to being placed on the MLS. If the strategy works, the broker gets paid a double commission and the seller will have sold their property in a severely manipulated market situation in which demand was intentionally curtailed. In addition, the seller and buyer forfeit their right to representation.

b. Internet Marketing Plan Manipulation (click here for story). Some firms have actually pulled their sellers’ listings from the top buyer frequented real estate websites in order to collect double commissions.

Solution. Walk away from any brokerage firm that encourages you to do a pocket listing or excludes third-party internet websites from their marketing plan. Only use brokerage firms that offer a complete marketing plan that includes their listings on Realtor.com, Zillow, Trulia, MSN RealEstate, Yahoo Real Estate, NeighborCity.com, and others.

6. Buyer Broker Compensation (click here to learn how to negotiate your buyer broker’s fee). Buyer brokers typically get paid by the seller which creates a horrible conflict of interest. Combine that with the fact that the listing broker actively conceals this offer of compensation from both the buyer and seller and the result can be outright bribery. Many listing companies and builders will provide huge secret incentives to buyer brokers who are successful in convincing buyers to purchase their listings.

Solution. Use a small brokerage and hire the broker (they don’t have to split their commission with agents). Negotiate your buyer broker’s fee upfront and before you are shown any properties. Insist that your broker disclose all compensation being offered prior to showing you any house. Insist that your broker pay all seller or listing broker incentives to you.

7. Open Houses (click here for story). Open houses do not even make the list of effective ways to sell a house. Open houses are traps for home buyers and sellers that foster dual agency and double commissions. Walking into an open house could easily result in a commission dispute if the buyer decides that they want to hire their own broker to negotiate the transaction. As a result, it is likely that the buyer will forfeit both their and the seller’s right to representation. Open houses serve no purpose other than to provide the listing broker with a free platform to solicit buyer clients to find other homes. They also create a security risk for sellers.

Solution. Do not let your Realtor hold ANY open houses and do not go to any open houses.

8. Bad Forms (click here for Consumer-Friendly Listing Contract) (click here for Consumer-Friendly Seller Representation Clauses) (Click here for Consumer-Friendly Buyer Representation Clauses). The negotiating power of buyers and sellers are ignored in the industry forms (mostly drafted by Realtor Associations). The forms that exist include many unsavory elements to which no consumer should ever agree. Extra fees and commissions payable even if the deal does not close are two examples.

Solution. Use a small brokerage firm that is willing to negotiate their contract (large firms rarely do.) Hire an attorney to help negotiate this key form.

9. Home Warranties (click here for story). Home warranties are rarely worth the expense and provide secret incentives to real estate brokers and agents. There exists so much misinformation about home warranties that a google search of “problems with home warranties” now leads you to many self-serving blogs. Try searching “home warranty rip-offs” or go to sites like the Ripoff Report. Many Realtor Associations have now included a checkbox for buyers to select the purchase agreement requiring the seller to pay for a home warranty as part of the transaction.

Solution. Do not buy or sell a home warranty. If a home warranty is required as part of the transaction, require your broker to pay you the compensation that they would have collected for selling this.

10. Arbitration (click here and see clause 8). Many Realtors advise their buyers and sellers to agree to arbitration if a dispute arises in the transaction. Arbitration only benefits the broker in that it reduces their liability. The act of advising a client to agree to arbitration is most likely the unauthorized practice of law reserved for lawyers, not Realtors. Arbitration usually costs a lot more than Small Claims court, has a reduced statute of limitations and the arbitrators are often unqualified and sometimes biased.

Solution. Do not ever sign the arbitration clause unless your attorney advises you to do so.

Bonus 11. Bad Laws. Realtor Associations are the top lobbyists in the country (click here for the link to statistics) and that comes with a high price tag for consumers. Whether it be the one year statute of limitations on RESPA violations (most laws have a 6 year statute of limitations) or states that legalized the price fixing of buyer broker fees, the fact is that there are an unreasonably large number of anti-consumer laws that serve to abrogate common law rights and manipulate licensing and regulatory laws to protect brokerage firms from consumer legal actions.

Solution. Sign our petitions(petition to eliminate the ban on broker fee negotiations in 11 states) (petition to increase anti-kickback statute of limitations from 1 year to 6) to help change some of these laws and tell us your stories by clicking on Talk To Us.

*National Association of Realtors Survey.