National Consumer Alert – for Buyers and Sellers

Avoid Nationwide Open House Weekend

CAARE is releasing this consumer alert to warn home buyers and sellers to avoid the Nationwide Open House weekend being promoted by the National Association of Realtors (“NAR”). Open houses are proven consumer traps for both buyers and sellers and they substantially increase sellers’ exposure to criminal activity. Open houses are great for brokers and rookie agents to find new leads on clients not interested in the specific open house.

Seller Warning

Security Risk to Sellers

It is well documented that theft and even violent crimes often occur at open houses. Publishing an open house is an invitation to criminals and provides a unique opportunity for criminals to case a home for a future crime or commit a crime while someone else distracts the onsite Realtor. NAR does not mention this risk in their promotions. Realtor listing contracts exclude liability for thefts that occur at open houses.

Open Houses Do Not Sell Houses

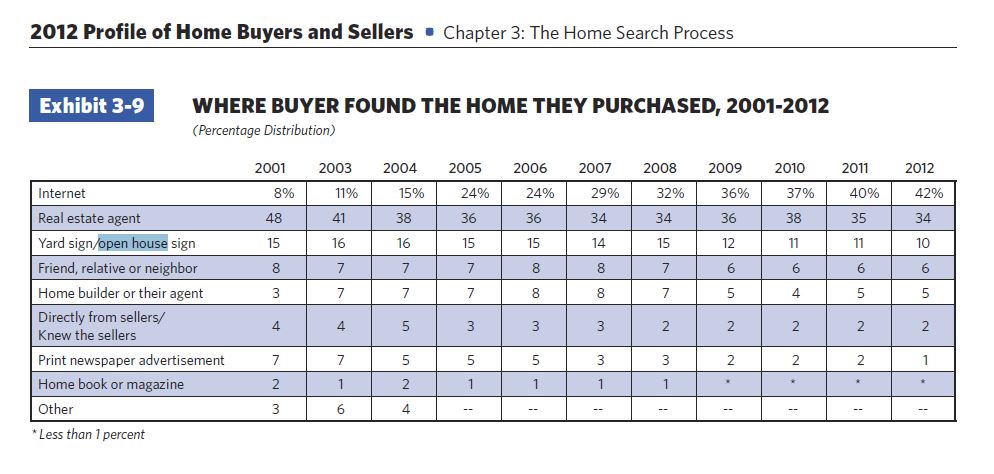

“Only a small percentage of homes are sold through open houses 1.” NAR’s survey unfortunately combines their “statistics” on open house “signs” with yard signs. The problem is that yard signs alone are a very successful tool to sell houses and open houses are not. The NAR survey inquires about open house “signs,” rather than the open houses themselves, which creates ambiguity in the results. On a scale of 1 to 5 (with “5” being very effective and “1” being not effective at all), top real estate agents rated yard signs as the top selling tool (above the MLS) with a rating of 4.68 and placed open houses 10th on the list with a score of 2.88 2. Together, yard signs and open house signs accounted for 10% of how buyers found their homes (See exhibit 3-9 below 3. ). We suspect that open houses account for less than 1% of home sales. One of our members attended a continuing education class in which the instructor proclaimed that open houses serve one purpose – to find buyers to buy other houses.

Buyer Warning

According to NAR, “Potential home buyers rely on open houses to help them find the home of their dreams. ” We find this statement misleading because most home buyers do not find the home that they are going to purchase by visiting open houses.

Open Houses are Traps

Buyers who enter an open house are often unknowingly giving up their right to hire a buyer broker of their choice. That means that they lose the right to have someone provide important negotiating advice on price and terms. If the seller’s broker feels that they are the procuring cause of the sale, they can refuse to share their commission with your buyer broker. Since buyer brokers get paid from the seller’s broker, that creates a problem for buyers.

Rookie Agents from Mega Firms Work Most Open Houses

Open houses are often training grounds for rookie agents who possess little expertise. Most open houses are run by large listing firms that have conflicts of interests that negatively affect buyers. Buyers should not use open houses to find an agent.

Do It Yourself Buyers

Some buyers want to find their home themselves and visit open houses as part of the process. Unlike sellers who save thousands of dollars if they sell their house themselves, buyers save nothing unless they know how to negotiate for the commission offered to buyer brokers. Sellers brokers love do it yourselfers because they often turn them into a double commission pay out. See CAARE’s Open House Form (click here).

[1] Home Sellers Handbook – Minnesota Attorney General’s Office

[2] Survey Slams Door on Open Houses. CRSs Pick Favorite Listing, Selling Techniques

[3]